都搜索不到了

Q:有微信群,QQ群吗?

A:vn.py框架学习群:666359421 ; vn.py框架交流群:262656087

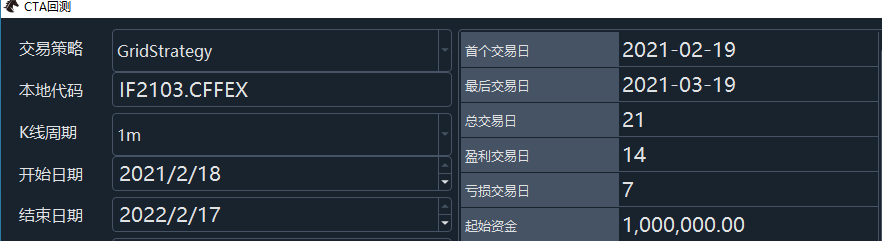

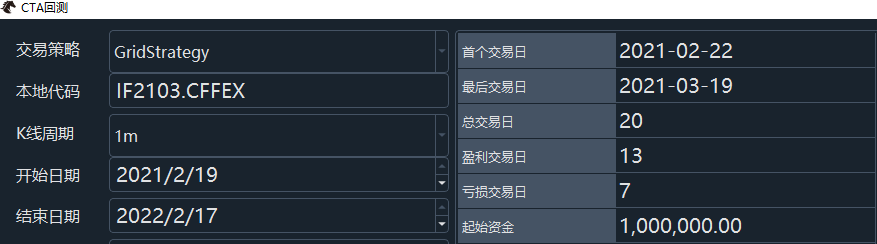

自己写了一个策略,回测时总是没有回测起始日数据,请问可能是什么原因呢?按照策略逻辑,肯定是应该有交易的。比如下图,策略从19日开始,首个交易日就是22日,19日无交易,但是我把回测日期调到18日开始,19日就有交易了。

CSV分钟线也是从VNPY导出来的(另外一台电脑的),新导入了(2.9.0版本)就出错。

不用导入,直接用udata下载的话,也是报这个错误。VNPY是卸载了原来的2.5版本,新安装的2.9版本。请问是怎么回事呢?

Traceback (most recent call last):

File "c:\vnstudio\lib\site-packages\peewee.py", line 3160, in execute_sql

cursor.execute(sql, params or ())

sqlite3.OperationalError: table dbbardata has no column named turnover

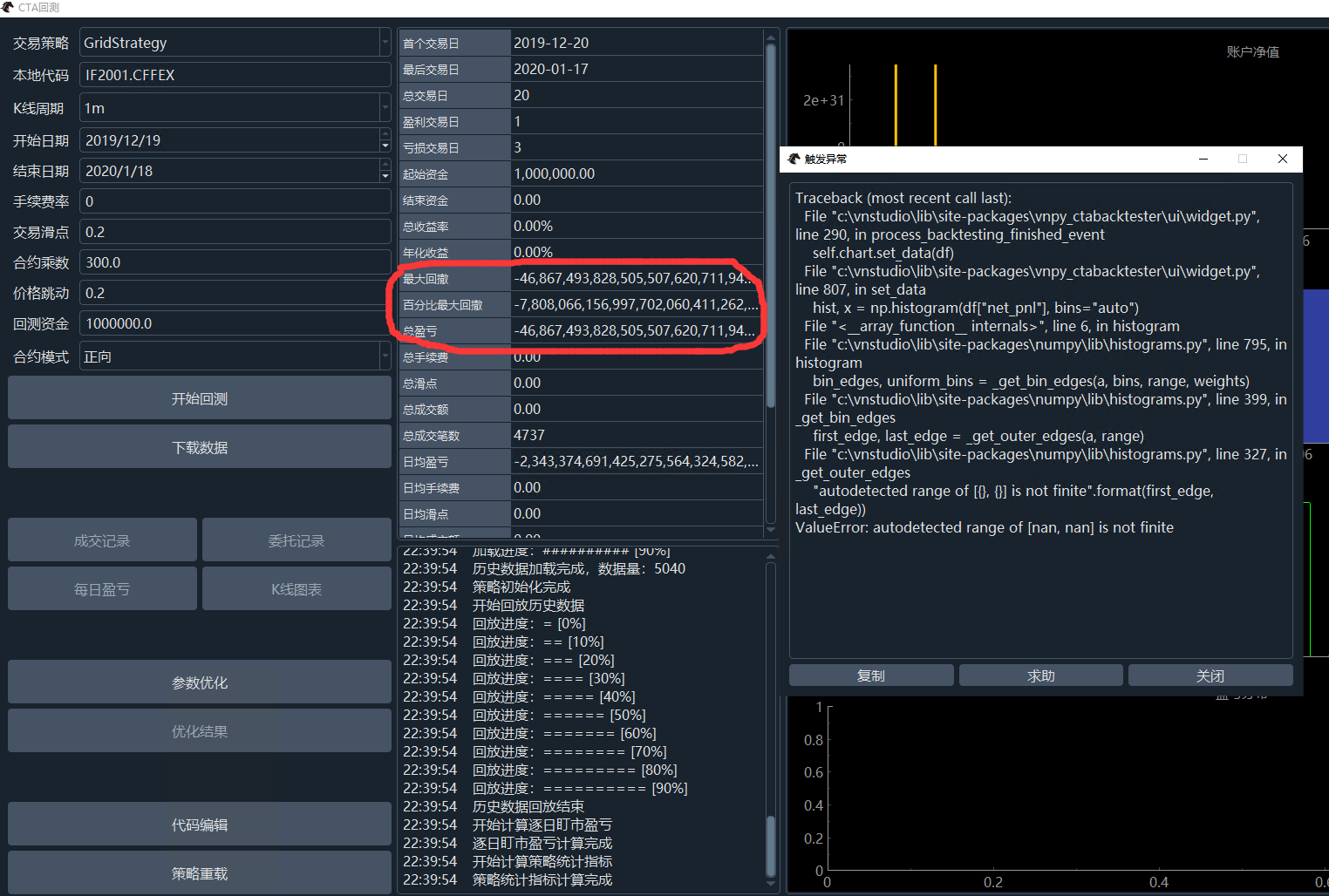

写了一个网格交易的策略,回测的时候,最大回撤都无穷大了,请问是怎么回事呢?

from vnpy.app.cta_strategy import (

CtaTemplate,

StopOrder,

TickData,

BarData,

TradeData,

OrderData,

BarGenerator,

ArrayManager,

)

import math

class GridStrategy(CtaTemplate):

""""""

author = "Fighter"

#定义参数

initial_price = 1.0

step_price = 1.0

step_volume = 1.0

max_pos = 4

vt_orderid = ""

pos = 0

parameters = ["initial_price", "step_price", "step_volume", "max_pos"]

variables = ["pos", "vt_orderid"]

def __init__(self, cta_engine, strategy_name, vt_symbol, setting):

""""""

super().__init__(cta_engine, strategy_name, vt_symbol, setting)

self.bg = BarGenerator(self.on_bar)

self.am = ArrayManager()

def on_init(self):

"""

Callback when strategy is inited.

"""

self.write_log("策略初始化")

self.load_bar(1)

self.pos = 0

def on_start(self):

"""

Callback when strategy is started.

"""

self.write_log("策略启动")

self.put_event()

def on_stop(self):

"""

Callback when strategy is stopped.

"""

self.write_log("策略停止")

self.put_event()

def on_tick(self, tick: TickData):

"""

Callback of new tick data update.

"""

self.bg.update_tick(tick)

def on_bar(self, bar: BarData):

"""

Callback of new bar data update.

"""

#self.bg.update_bar(bar)

#self.cancel_all()

am = self.am

am.update_bar(bar)

if not am.inited:

return

if self.initial_price > bar.close_price:

# 价格在基准价之上时

# 计算当前K线收盘价与初始价的距离

target_buy_distance = (self.initial_price - bar.close_price) / self.step_price

# 计算当前价位应该持有的仓位,取整。再和最大仓位置比较

target_buy_position = min(math.floor(target_buy_distance) * self.step_volume, self.max_pos)

# 当前应该持有的仓位减去原有持仓就是该再买入的仓位

target_buy_volume = target_buy_position - self.pos

# Buy when price dropping

if target_buy_volume > 0:

self.buy(bar.close_price, target_buy_volume)

# Sell when price rising

elif target_buy_volume < 0:

self.sell(bar.close_price, target_buy_volume)

elif self.initial_price < bar.close_price:

# 价格在基准价之下时

target_buy_distance = (bar.close_price - self.initial_price) / self.step_price

target_buy_position = - min(math.floor(target_buy_distance) * self.step_volume, self.max_pos)

target_buy_volume = target_buy_position - self.pos

# Buy when price dropping

if target_buy_volume > 0:

self.buy(bar.close_price, target_buy_volume)

# Sell when price rising

elif target_buy_volume < 0:

self.sell(bar.close_price, target_buy_volume)

# Update UI

#self.put_variables_event()

def on_order(self, order: OrderData):

"""

Callback of new order data update.

"""

pass

def on_trade(self, trade: TradeData):

"""

Callback of new trade data update.

"""

self.put_event()

def on_stop_order(self, stop_order: StopOrder):

"""

Callback of stop order update.

"""

passGitHub安装后的功能要少一些呢

用行情记录来记录价差的tick。

谢谢指导!

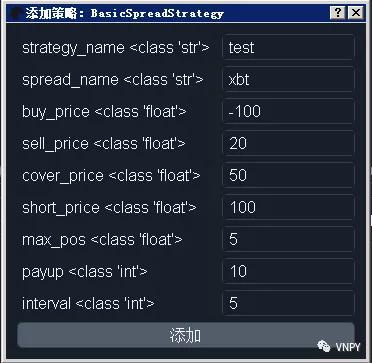

buy_price/sell_price/cover_price/short_prie:四个方向的交易价格,比如buy_price 是看价差中的买价还是卖价呢?

实际建仓的时候,实际上是以建立的价差中的卖价成交的。平仓的时候,又是以建立的价差中的买价成交的。

查了一下,说可能是网络读失败,APP版本和服务器备案版本不对。

该怎么改呢?

我是按照教程填写的

用户名username:111111 (6位纯数字账号)

密码password:1111111 (需要修改一次密码用于盘后测试)

经纪商编号brokerid:9999 (SimNow默认经纪商编号)

交易服务器地址td_address:218.202.237.33 :10102 (盘中测试)

行情服务器地址md_address:218.202.237.33 :10112 (盘中测试)

授权码auth_code:0000000000000000(16个0)

名称app_id:simnow_client_test