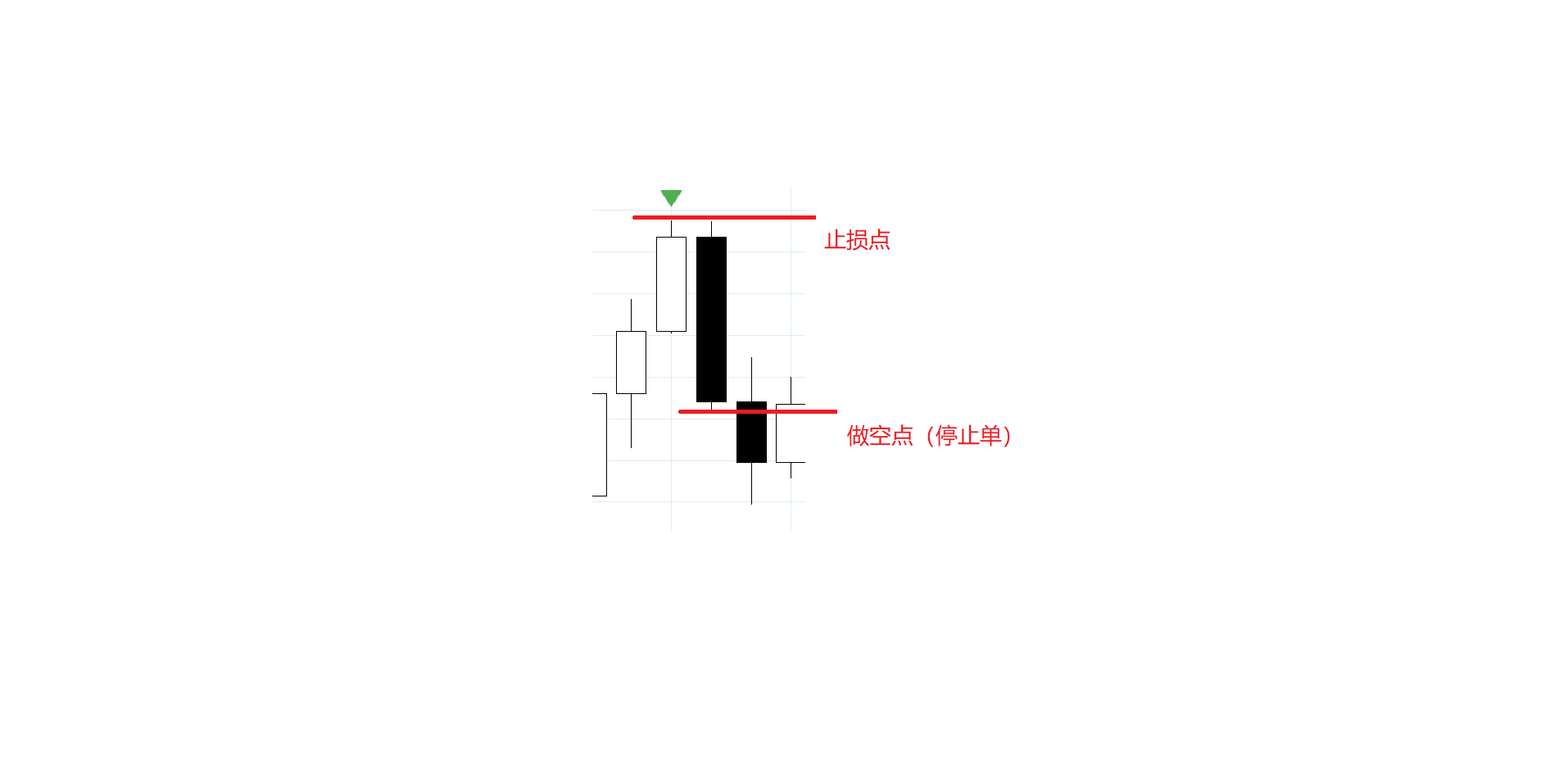

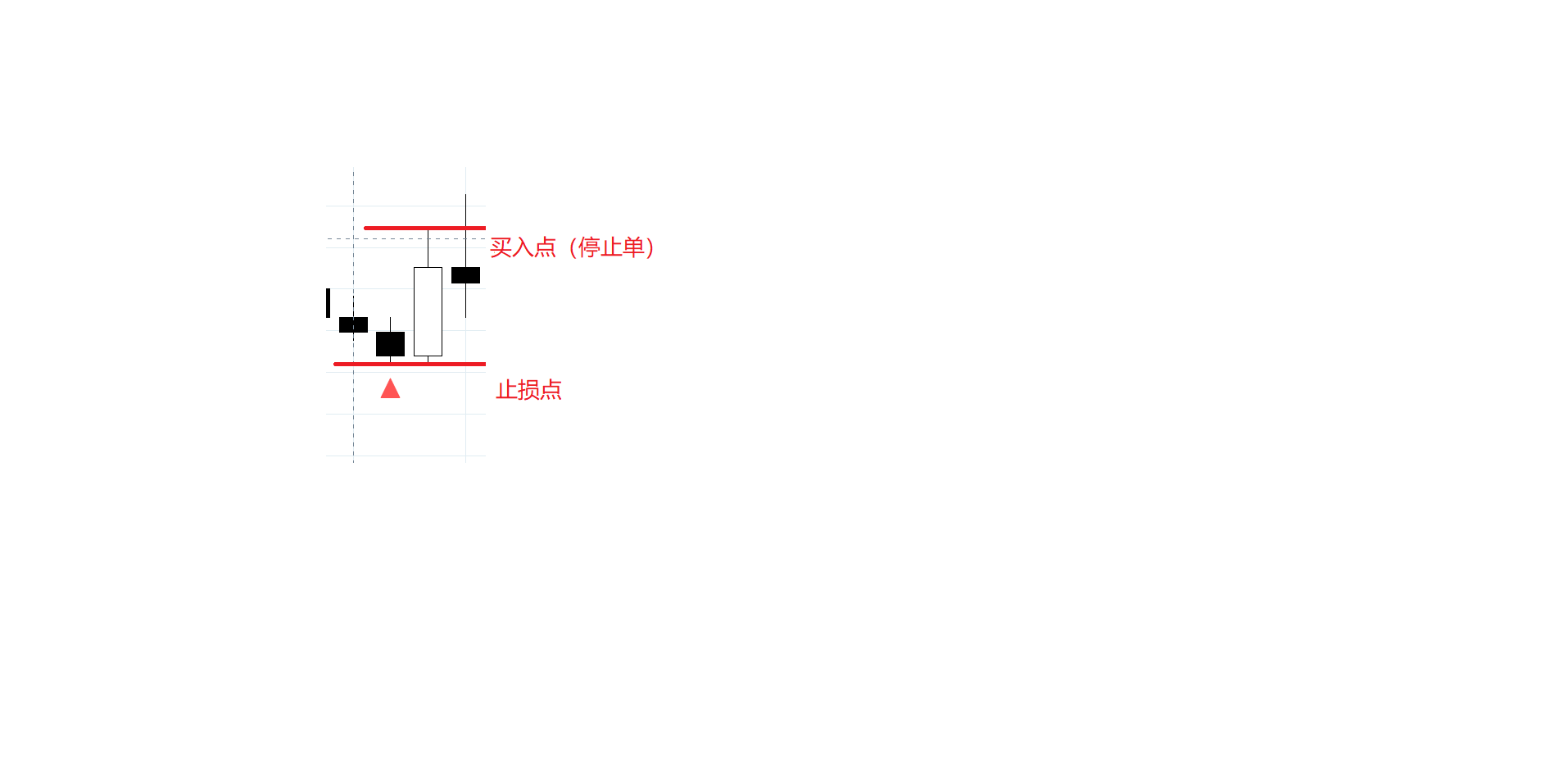

写了一个很简单的“黎明之星”的蜡烛形态策略(多空点以及止盈止损位置如下图所示)

入场方式用的是停止单。但是策略跑出来后,开仓点,止盈,止损都是乱七八糟的。求大家帮忙看下我哪里出问题了,感激!!

from vnpy.app.cta_strategy import (

CtaTemplate,

StopOrder,

TickData,

BarData,

TradeData,

OrderData,

BarGenerator,

ArrayManager,

)

from vnpy.trader.constant import Interval

class morning_star(CtaTemplate):

author = "Leo_Monster"

fixed_size=1

wining_ratio=1.1

sl_pip=0.00050

sl_entry_long=0

sp_entry_long=0

sl_entry_short=0

sp_entry_short=0

entry_price = 0

parameters = ['fixed_size','wining_ratio','sl_pip']

variables = ['sl_entry_long','sp_entry_long','sl_entry_short','sp_entry_short','entry_price']

def __init__(self, cta_engine, strategy_name, vt_symbol, setting):

super().__init__(cta_engine, strategy_name, vt_symbol, setting)

self.bg = BarGenerator(self.on_bar,window=1,interval=Interval.HOUR,on_window_bar=self.on_60min_bar)

self.am = ArrayManager()

def on_init(self):

"""

Callback when strategy is inited.

"""

self.write_log("策略初始化")

self.load_bar(5)

def on_start(self):

"""

Callback when strategy is started.

"""

self.write_log("策略启动")

self.put_event()

def on_stop(self):

"""

Callback when strategy is stopped.

"""

self.write_log("策略停止")

self.put_event()

def on_tick(self, tick: TickData):

"""

Callback of new tick data update.

"""

self.bg.update_tick(tick)

def on_order(self, order: OrderData):

"""

Callback of new order data update.

"""

pass

def on_trade(self, trade: TradeData):

"""

Callback of new trade data update.

"""

self.put_event()

def on_stop_order(self, stop_order: StopOrder):

"""

Callback of stop order update.

"""

pass

def on_bar(self, bar: BarData):

self.bg.update_bar(bar)

def on_60min_bar(self,bar: BarData):

am = self.am

am.update_bar(bar)

if not self.am.inited:

return

self.up_trend = self.am.low_array[-2] < self.am.low_array[-1] and\

self.am.low_array[-2] < self.am.low_array[-3] and\

self.am.high_array[-1] > self.am.high_array[-2] and\

self.am.high_array[-3] > self.am.high_array[-2]

self.down_trend = self.am.high_array[-2] > self.am.high_array[-3] and\

self.am.high_array[-2] > self.am.high_array[-1] and\

self.am.low_array[-3] < self.am.low_array[-2] and\

self.am.low_array[-1] < self.am.low_array[-2]

if self.pos == 0:

if self.up_trend:

self.entry_price=self.am.high_array[-1]

self.sl_entry_long=self.am.low_array[-2] #做多 止盈点

self.sp_entry_long=self.am.high_array[-1]+abs(self.am.high_array[-1]-self.am.low_array[-2]) #做空 止损点

self.buy(self.entry_price,1,True) #做多头仓位

self.sell(self.sl_entry_long,abs(self.pos),True)#止损

self.sell(self.sp_entry_long,abs(self.pos)) #止盈

if self.down_trend:

self.entry_price=self.am.low_array[-1]

self.sl_entry_short=self.am.high_array[-2] #做空 止盈点

self.sp_entry_short=self.am.low_array[-1]+abs(self.am.high_array[-2]-self.am.low_array[-1]) #做空 止损点

self.sell(self.entry_price,1,True) #做空头仓位

self.cover(self.sl_entry_short,abs(self.pos),True) #止损

self.cover(self.sp_entry_short,abs(self.pos)) #止盈

if self.pos < 0:

if self.up_trend:

self.entry_price=self.am.high_array[-1] #入场价

self.sl_entry_long=self.am.low_array[-2] #做多 止盈点

self.sp_entry_long=self.am.high_array[-1]+abs(self.am.high_array[-1]-self.am.low_array[-2]) #做空 止损点

self.cover(bar.close_price,abs(self.pos)) #平空头仓

self.buy(self.entry_price,1,True) #做多头仓位

self.sell(self.sl_entry_long,abs(self.pos),True) #止损

self.sell(self.sp_entry_long,abs(self.pos)) # 止盈

if self.down_trend:

self.entry_price=self.am.low_array[-1] #入场价

self.sl_entry_short=self.am.high_array[-2] #做空 止盈点

self.sp_entry_short=self.am.low_array[-1]+abs(self.am.high_array[-2]-self.am.low_array[-1]) #做空 止损点

self.cover(bar.close_price,abs(self.pos)) #平掉之前所持有的空头仓

self.sell(self.entry_price,1,True) #再做空

self.cover(self.sl_entry_short,abs(self.pos),True) #止损

self.cover(self.sp_entry_short,abs(self.pos)) #止盈

if self.pos > 0:

if self.up_trend:

self.entry_price=self.am.high_array[-1]

self.sl_entry_long=self.am.low_array[-2] #做多 止盈点

self.sp_entry_long=self.am.high_array[-1]+abs(self.am.high_array[-1]-self.am.low_array[-2]) #做空 止损点

self.sell(bar.close_price,abs(self.pos)) #平掉之前的多头仓

self.buy(self.entry_price,1,True) #再开一个多头仓

self.sell(self.sl_entry_long,abs(self.pos),True) #止损

self.sell(self.sp_entry_long,abs(self.pos)) #止盈

self.buy(bar.close_price,1)

if self.down_trend:

self.entry_price=self.am.low_array[-1] #入场价

self.sl_entry_short=self.am.high_array[-2] #做空 止盈点

self.sp_entry_short=self.am.low_array[-1]+abs(self.am.high_array[-2]-self.am.low_array[-1]) #做空 止损点

self.sell(bar.close_price,abs(self.pos)) #平多头仓位

self.sell(self.entry_price,1,True) # 下空头仓位

self.cover(self.sl_entry_short,abs(self.pos),True) #止损

self.cover(self.sp_entry_short,abs(self.pos)) #止盈

self.put_event()青青子荆 wrote:

- 删掉def on_bar()后面的normal

- 你用了小时的bar,因此需要在策略文件前面加上一行 from vnpy.trader.constant import Interval

这就去试一下,非常感谢!!!

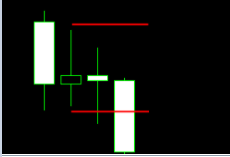

大家好,我是名正在不断摸索学习的 “小学生“ 。 最近遇到了点小问题。我尝试写一个price action类型的策略(如下图所示)

当最新一根K线突破内包线(inside bar)的时候,就做空或者做多;处于着急测试的原因,我这个策略只写了做多部分。

问题就是:

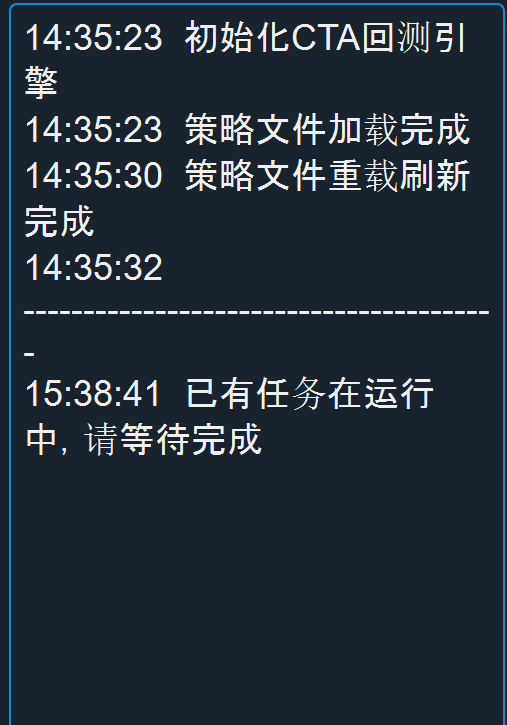

当我打开vnpy ui进行回测的时候,无法进行回测(如下图所示)

等了很长时间没有反应就又点了一下回测,就显示这样的图片

但当我不通过打开vnpy客户端而是用backtesting文件回测的时候,却是可以跑的。

为了防止是数据方面的问题,我用同样的数据测试了下自带的几个strategy,并没有问题,所以问题肯定出在我写的这个代码上了。(我把代码attach在下面了)个人猜测会不会是因为我调用K线的方式有问题导致数据没法读取?

求各位大神们指点下。万分感谢

Regards,

Leo

from vnpy.app.cta_strategy import (

CtaTemplate,

StopOrder,

TickData,

BarData,

TradeData,

OrderData,

BarGenerator,

ArrayManager,

)

class three_bar(CtaTemplate):

author = "Leo_Monster"

fixed_size=1

parameters=["fixed_size"]

variables=[]

def __init__(self, cta_engine, strategy_name, vt_symbol, setting):

super().__init__(cta_engine, strategy_name, vt_symbol, setting)

self.bg = BarGenerator(self.on_bar,window=1,interval=Interval.HOUR)

self.am = ArrayManager()

def on_init(self):

"""

Callback when strategy is inited.

"""

self.write_log("策略初始化")

self.load_bar(5)

def on_start(self):

"""

Callback when strategy is started.

"""

self.write_log("策略启动")

def on_stop(self):

"""

Callback when strategy is stopped.

"""

self.write_log("策略停止")

def on_tick(self, tick: TickData):

"""

Callback of new tick data update.

"""

self.bg.update_tick(tick)

def on_bar(self, bar: BarData): normal

self.am.update_bar(bar)

if not self.am.inited:

return

if self.pos ==0:

if self.am.high_array[-2]>self.am.high_array[-1] and\

self.am.low_array[-2]<self.am.low_array[-1]:

self.buy(bar.open_price,self.fixed_size)

def on_order(self, order: OrderData):

"""

Callback of new order data update.

"""

pass

def on_trade(self, trade: TradeData):

"""

Callback of new trade data update.

"""

self.put_event()

def on_stop_order(self, stop_order: StopOrder):

"""

Callback of stop order update.

"""

pass不好意思刚开始学习,想请问下如何下载oanda外汇历史数据的?我使用策略回测的时候显示历史数据下载失败。。

求帮忙解答一下感激!!