某策略的回测结果

2021-07-19 20:42:13.439225 起始资金: 10,000,000.00

2021-07-19 20:42:13.439261 结束资金: 15,559,877.94

2021-07-19 20:42:13.439272 总收益率: 55.60%

2021-07-19 20:42:13.439280 年化收益: 79.90%

2021-07-19 20:42:13.439287 最大回撤: -3,004,434.58

2021-07-19 20:42:13.439295 百分比最大回撤: -17.23%

初始资金1000w

策略以固定手数进行交易

策略算得最大回撤是百分比大约是17%

但最大回撤值是300w

实际上是不是最大回撤值更有参考意义

如果从发生最大回撤前的高点开始交易

测得的最大回撤百分比将可能是30%

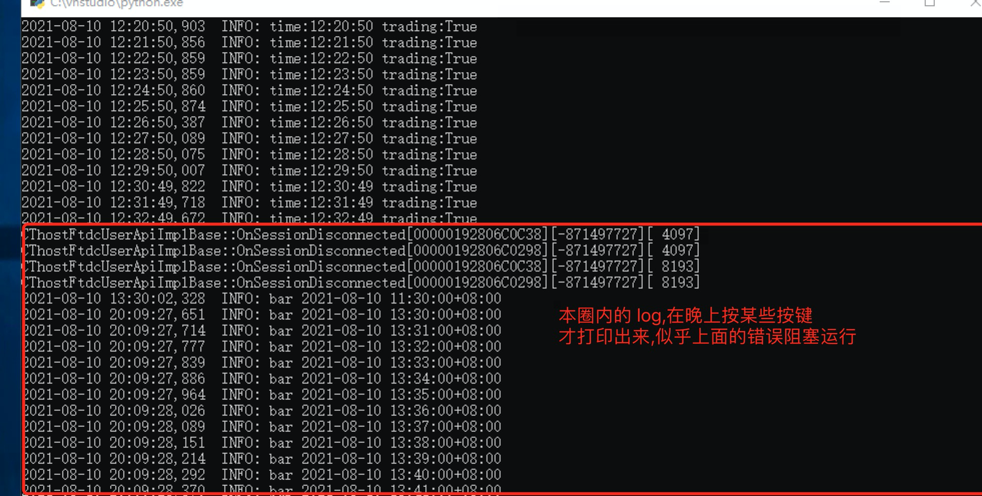

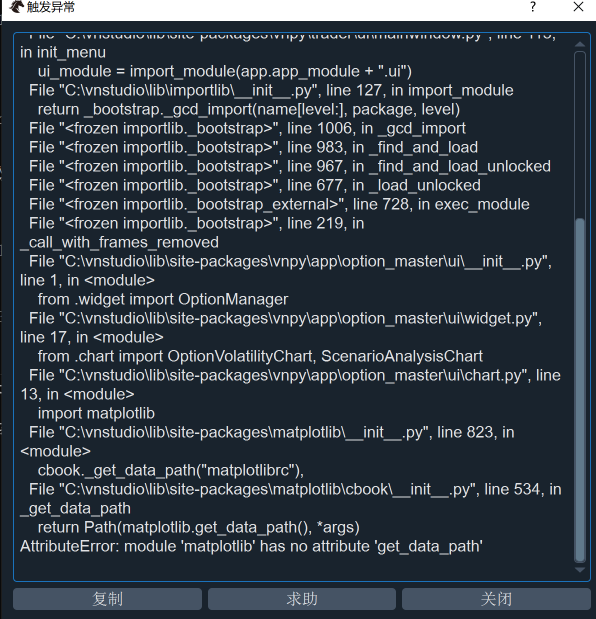

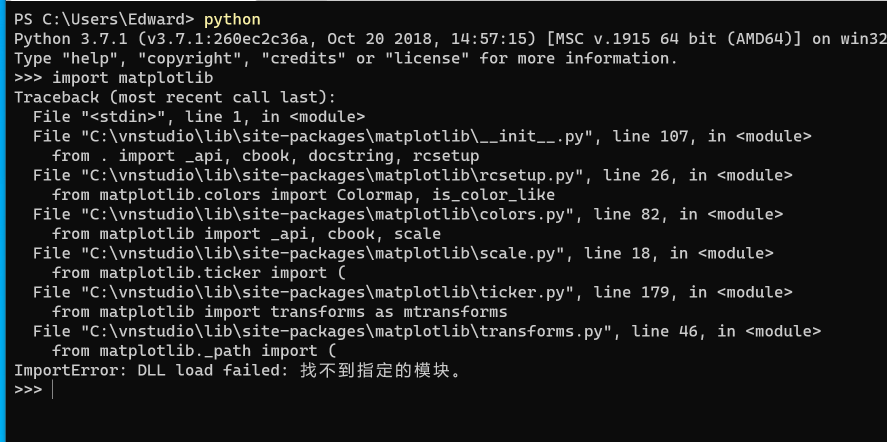

通过脚本启动,导入 matplotlib 错误

后来发现直接导入 matplotlib 也不错

以 i 铁矿为例

在我们开发阶段时大都使用 i99 (指数)或i888 (连续合约,前复权平滑)

在实盘时我们是不是应该继续使用i99或i888计算指标,而交易的是实际的标的如 i2201

因为发现有个问题,主力刚换月时,如果用主力的合约的数据去计算指标

得到指标有点奇怪,因为新主力之前的交易量太小,走势也不明显

欢迎发表意见~

例如

def on_init(self):

"""

Callback when strategy is inited.

"""

self.write_log("策略初始化")

self.load_bar(10)

会在数据回放时刚好漏掉达到10时的数据

例如:

2010-01-14 14:58:00+08:00

2010-01-14 14:59:00+08:00

2021-07-31 22:35:04.157915 策略初始化完成

2021-07-31 22:35:04.159658 开始回放历史数据

[这里缺少了2010-01-15 09:00:00+08:00]

2010-01-15 09:01:00+08:00

源码:backtesting_data少取了刚好达到阈值时的数据

# Use the rest of history data for running backtesting

backtesting_data = self.history_data[ix + 1:]

if not backtesting_data:

self.output("历史数据不足,回测终止")

return没有找到 load_ticks函数

from datetime import datetime, time

from config.common import log

from config.const import WEEK_DICT

DAY_START = time(8, 45)

DAY_END = time(15, 0)

NIGHT_START = time(20, 45)

NIGHT_END = time(2, 45)

WEEKEND_START = 6

today = datetime.now().weekday() + 1

def is_trading_time():

""""""

current_time = datetime.now().time()

trading = False

if (today < WEEKEND_START):

if (

(current_time >= DAY_START and current_time <= DAY_END)

or (current_time >= NIGHT_START)

or (current_time <= NIGHT_END)

):

trading = True

time = current_time.strftime("%H:%M:%S")

log.info("time:" + time + ' trading:' + str(trading))

return trading

def run_child():

"""

Running in the child process.

"""

SETTINGS["log.file"] = True

SETTINGS.update()

event_engine = EventEngine()

main_engine = MainEngine(event_engine)

main_engine.add_gateway(CtpGateway)

cta_engine = main_engine.add_app(CtaStrategyApp)

main_engine.write_log("主引擎创建成功")

log_engine = main_engine.get_engine("log")

event_engine.register(EVENT_CTA_LOG, log_engine.process_log_event)

main_engine.write_log("注册日志事件监听")

main_engine.connect(ctp_setting, "CTP")

main_engine.write_log("连接CTP接口")

sleep(10)

cta_engine.init_engine()

main_engine.write_log("CTA策略初始化完成")

cta_engine.init_all_strategies()

sleep(60) # Leave enough time to complete strategy initialization

main_engine.write_log("CTA策略全部初始化")

cta_engine.start_all_strategies()

main_engine.write_log("CTA策略全部启动")

while True:

sleep(60)

trading = time_util.is_trading_time()

if not trading:

cta_engine.stop_all_strategies()

log.info("关闭子进程")

sleep(60)

main_engine.close()

sleep(30)

sys.exit(0)

if name == "main":

run_child()

/Users/fourdirections_vincenttang/opt/miniconda3/lib/python3.7/site-packages/vnpy/app/cta_strategy/backtesting.py:472: RuntimeWarning: divide by zero encountered in double_scalars

return_drawdown_ratio = -total_return / max_ddpercent

遇到从由 tick 数据合成 分钟 bar 时,bar 数据没有成功取得最高价的问题

从 vnpy.trader.utility.py 中提取的代码

if new_minute:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

else:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

if tick.high_price > self.last_tick.high_price:

self.bar.high_price = max(self.bar.high_price, tick.high_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

if tick.low_price < self.last_tick.low_price:

self.bar.low_price = min(self.bar.low_price, tick.low_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

按当前算法,当第一个 tick的 last_price < high_price ,并且该high_price是一分钟内最大值时,

合成的分钟 bar 的 high_price 将会小于 该一分钟内实际的最大值

同理,当第一个 tick 的 last_price < low_price ,并且该low_price是一分钟内的最小值时,

合成的分钟 bar 的 low_price 将会大于该一分钟内实际的最小值

自带的DualThrustStrategy

使用

if last_bar.datetime.date() != bar.datetime.date():

作为新的一天的 k 线的判断条件,是否和平常使用的不一样

平时新的一天的 k 线都是以从夜盘开始的

尝试把CincoStrategy 用 tick 回测

on_tick 没有回调

反而 on_bar 有回调,但传过来的是DbTickData的对象

回测异常:

AttributeError: 'DbTickData' object has no attribute 'close_price'

回测程序如果下:

def run_backtesting(strategy_class, setting, vt_symbol, interval, start, end, rate, slippage, size, pricetick, capital):

engine = BacktestingEngine()

engine.set_parameters(

vt_symbol=vt_symbol,

interval=interval,

start=start,

end=end,

rate=rate,

slippage=slippage,

size=size,

pricetick=pricetick,

mode=BacktestingMode.TICK,

capital=capital

)

engine.add_strategy(strategy_class, setting)

engine.load_data()

engine.run_backtesting()

df = engine.calculate_result()

engine.calculate_statistics()

engine.show_chart()

return df

if name == "main":

df = run_backtesting(

strategy_class=CincoStrategy,

setting={},

vt_symbol="IF1912.CFFEX",

interval=Interval.TICK,

start=datetime(2019, 11, 25),

end=datetime(2019, 11, 26),

rate=0.3 / 10000,

slippage=0.2,

size=300,

pricetick=0.2,

capital=1_000_000,

)组合策略怎么实现停止单

portfolio_strategy 包的 template 没有提供 stop 参数选项

请问simnow的结果有多大的参考价值

看FAQ时看到:停止单到触发价时会以市价发单以实现最大的可能成交

问题一:

停止单有提供非市价发单的接口吗? 还是要自己实现

问题二:

比如从rqdata 使用1m 的数据回测

回测时使用停止单,这是不是和实盘情况有较大的差别,

回测时会以开盘成交对吧,实盘时会在k线内触发

simonw 行情中断过,然后的逻辑的就乱了(似乎bar的时间与pos的值都不对)

策略是此前分享的R_Breaker ,在update_bar 会调用cancel_all

问题

1:过程中连续开了两个1手多单,

2:有委托没找到

3:在最后收盘时也没有平仓

这些问题在实盘中可能遇到吗

self.tend_high, self.tend_low = am.donchian(self.donchian_window)

if bar.datetime.time() < self.exit_time:

if self.pos == 0:

self.intra_trade_low = bar.low_price

self.intra_trade_high = bar.high_price

if self.tend_high > self.sell_setup:

long_entry = max(self.buy_break, self.day_high)

self.buy(long_entry, self.fixed_size, stop=True)

self.short(self.sell_enter, self.multiplier * self.fixed_size, stop=True)

elif self.tend_low < self.buy_setup:

short_entry = min(self.sell_break, self.day_low)

self.short(short_entry, self.fixed_size, stop=True)

self.buy(self.buy_enter, self.multiplier * self.fixed_size, stop=True)

elif self.pos > 0:

self.intra_trade_high = max(self.intra_trade_high, bar.high_price)

long_stop = self.intra_trade_high * (1 - self.trailing_long / 100)

self.sell(long_stop, abs(self.pos), stop=True)

elif self.pos < 0:

self.intra_trade_low = min(self.intra_trade_low, bar.low_price)

short_stop = self.intra_trade_low * (1 + self.trailing_short / 100)

self.cover(short_stop, abs(self.pos), stop=True)

else:

if self.pos > 0:

self.sell(bar.close_price 0.99, abs(self.pos))

elif self.pos < 0:

self.cover(bar.close_price 1.01, abs(self.pos))