最近发现quantaxis的1分钟数据7万条数据耗时0:00:00.001997

+

但是vnpy的database_manager.load_bar_data,提取7万条数据要10秒钟,所以想着手改造一下,

+

但是我发现quantaxis用的是pymongo的collection.insert_many()方法存数据,collection.find()方法读取数据,在vnpy的数据库源代码却找不到相关的方法,所以想问下各位大佬vnpy的MongoDB连接是不是基于pymongo写的?有没有可能优化后达到quantaxis的提取速度?

+

def load_bar_data(

self,

symbol: str,

exchange: Exchange,

interval: Interval,

start: datetime,

end: datetime,

collection_name: str = None,

) -> Sequence[BarData]:

if collection_name is None:

s = DbBarData.objects(

symbol=symbol,

exchange=exchange.value,

interval=interval.value,

datetime__gte=start,

datetime__lte=end,

)

else:

with switch_collection(DbBarData, collection_name):

s = DbBarData.objects(

symbol=symbol,

exchange=exchange.value,

interval=interval.value,

datetime__gte=start,

datetime__lte=end,

)

data = [db_bar.to_bar() for db_bar in s]

return datavnpy代码上面没有pymongo的影子。

大佬们,我是装了发行版2.1.7在C盘,同时我在D盘搞了个源代码文件夹vnpy2.1.7(里面也有vnpy文件夹),pycharm的解释器路径设置的是c盘vnpy的发行版安装的那个python.exe。

+

+

现在我在D盘的vnpy2.1.7文件夹,把里面的vnpy文件夹代码改了很多(包括MongoDB分表储存、成交额因子等等记不清了)

+

我在D盘的vnpy2.1.7文件夹下写的代码

from vnpy.event import EventEngine

from vnpy.trader.setting import SETTINGS

from vnpy.trader.engine import MainEngine

from vnpy.gateway.ctp import CtpGateway

from vnpy.app.cta_strategy import CtaStrategyApp

from vnpy.app.cta_strategy.base import EVENT_CTA_LOG上面这些代码引用的是C盘的发行版里面的vnpy库,还是D盘的VNPY2.1.7文件夹下面的vnpy文件件代码?

不太理解这个引用机制,请教下各位大佬!

我看很多地方离有注册如下事件:

def register_event(self):

""""""

# self.event_engine.register(EVENT_TICK, self.process_tick_event)

self.event_engine.register(EVENT_CONTRACT, self.process_contract_event)我理解这里是注册了一个EVENT_CONTRACT事件对应的处理函数,但是我想搞清楚EVENT_CONTRACT是哪个模块的哪个代码文件推出来的?

pandas的dataframe(从csv读取而来),在处理过程中,原来导入1min的是增加一列,这个写法运行无误

imported_data['interval'] = Interval.MINUTE+

现在想导入5min,以下写法均报错

imported_data['interval'] = 5*Interval.MINUTEimported_data['interval'] = “5min”请假该如何写这里的代码?感谢!(读取还没试,因为没保存进去)

看了许久,没研究清楚下面这个代码中哪里订阅合约?

+

我看所有的示例策略中都没有 合约 这个参数,示例策略中也没有订阅过程,也就是策略和合约是完全分离的。。。疑惑

+

def run_child():

"""

Running in the child process.

"""

SETTINGS["log.file"] = True

event_engine = EventEngine()

main_engine = MainEngine(event_engine)

main_engine.add_gateway(CtpGateway)

cta_engine = main_engine.add_app(CtaStrategyApp)

main_engine.write_log("主引擎创建成功")

log_engine = main_engine.get_engine("log")

event_engine.register(EVENT_CTA_LOG, log_engine.process_log_event)

main_engine.write_log("注册日志事件监听")

main_engine.connect(ctp_setting, "CTP")

main_engine.write_log("连接CTP接口")

sleep(10)

cta_engine.init_engine()

main_engine.write_log("CTA策略初始化完成")

cta_engine.init_all_strategies()

sleep(60) # Leave enough time to complete strategy initialization

main_engine.write_log("CTA策略全部初始化")

cta_engine.start_all_strategies()

main_engine.write_log("CTA策略全部启动")

while True:

sleep(10)

trading = check_trading_period()

if not trading:

print("关闭子进程")

main_engine.close()

sys.exit(0)尽量帮忙用代码指导,感激不尽!

+

需求:

合约交易时间:9:30-11:30及13:00-15:00

+

交易时间段内每分钟结束后的第5秒,触发一个事件。

+

上面这个需求不想通过on bar 里面的sleep5秒来实现(因为这样本质上还是bar事件逻辑,而非时间事件逻辑),我希望能实现策略能实现定时触发一个处理函数(时间事件逻辑)

+

感谢!!!!

`def QA_data_futuremin_resample20201205(

min_data,

type_='5min',

exchange_id=Exchange.CFFEX

):

"""期货分钟线采样成大周期

分钟线采样成子级别的分钟线

future:

vol ==> trade

amount X

期货一般两种模式:

中金所 股指期货: 9:30 - 11:30/ 13:00 -15:00

其他期货: -1 21:00: 2:30 / 9:00 - 11:30 / 13:30-15:00

输入demo

open high low close open_interest volume

datetime

2020-11-24 09:33:00+08:00 3465.9598 3466.3631 3463.9408 3465.0981 68138.0 588.0

2020-11-24 09:34:00+08:00 3465.5208 3470.3931 3464.5840 3469.7117 67968.0 676.0

2020-11-24 09:35:00+08:00 3469.9932 3470.6966 3466.8064 3468.5448 67851.0 427.0

2020-11-24 09:36:00+08:00 3468.4432 3470.1731 3463.9361 3464.2188 67684.0 431.0

2020-11-24 09:37:00+08:00 3464.0211 3464.3037 3456.2692 3457.5784 67481.0 532.0

2020-11-24 09:38:00+08:00 3457.8283 3457.8737 3451.8422 3453.3229 67163.0 603.0

2020-11-24 09:39:00+08:00 3453.7302 3456.1880 3453.2948 3455.7669 66960.0 358.0

2020-11-24 09:40:00+08:00 3455.5569 3455.6181 3450.4431 3450.4431 66642.0 568.0

"""

CONVERSION = {

# 'code': 'first',

'open': 'first',

'high': 'max',

'low': 'min',

'close': 'last',

# 'datetime': 'last',

'open_interest': 'last',

'volume': 'sum'

}

min_data = min_data.loc[:, list(CONVERSION.keys())]

idx = min_data.index

if exchange_id == Exchange.CFFEX:

part_1 = min_data.iloc[idx.indexer_between_time('9:30', '11:30')]

part_1_res = part_1.resample(

type_,

base=30,

closed='right',

loffset=type_

).apply(CONVERSION)

# part_2 = min_data.iloc[idx.indexer_between_time('13:00', '15:00')]

part_2 = min_data.iloc[idx.indexer_between_time('13:00', '15:15')]#为了适配中金所国债期货交易时间20201205

part_2_res = part_2.resample(

type_,

base=0,

closed='right',

loffset=type_

).agg(CONVERSION)

return pd.concat(

[part_1_res,

part_2_res]

# ).dropna().sort_index().reset_index().set_index(['datetime','code'])

).dropna().sort_index()

else:

part_1 = min_data.iloc[np.append(

idx.indexer_between_time('0:00',

'11:30'),

idx.indexer_between_time('0:00',

'11:30')

)]

part_1_res = part_1.resample(

type_,

base=0,

closed='right',

loffset=type_

).apply(CONVERSION)

part_2 = min_data.iloc[idx.indexer_between_time('13:30', '15:00')]

part_2_res = part_2.resample(

type_,

base=30,

closed='right',

loffset=type_

).agg(CONVERSION)

part_3 = min_data.iloc[idx.indexer_between_time('21:00', '23:59')]

part_3_res = part_3.resample(

type_,

base=0,

closed='right',

loffset=type_

).agg(CONVERSION)

return pd.concat(

[part_1_res,

part_2_res,

part_3_res]

# ).dropna().sort_index().reset_index().set_index(['datetime','code'])

).dropna().sort_index()`从MongoDB取数据出来 1年的1分钟bardata近6万条,取出来的时间大约10秒钟,请教一下各位大佬这是不是MongoDB的性能问题,如果想减少这个读取时间,就要换其他数据库?有什么推荐么?

备注:MongoDB数据已经分表储存。

1++++

首先在回测代码中通过引擎属性赋值参数如下:

#%%

engine = BacktestingEngine()

engine.set_parameters(

vt_symbol="IH99.CFFEX",

interval="1m",

start=datetime(2019, 6, 1),

end=datetime(2019, 6, 30),

rate=0.3/10000,

slippage=0.2*5,

size=300,

pricetick=0.2,

capital=1_000_000,

collection_name = "IH99"

)

engine.add_strategy(AtrRsiStrategy, {})+

+

2+++++

AtrRsiStrategy策略中onbar如下:

def on_bar(self, bar: BarData):

"""

Callback of new bar data update.

"""

self.cancel_all()

df01=load_select_bar_data_from_mongodb(self.symbol,self.exchange,self.interval,(bar.datetime-timedelta(days=3)),

bar.datetime,self.collection_name)

print (df01)

self.put_event()注:load_select_bar_data_from_mongodb是自定义的从MongoDB数据库读取bardata并生成dataframe的函数,有关于symbol等参数需要传入。

+

+

+

3++++++++++

回测运行报错如下:

2020-11-30 22:50:43.167187 Traceback (most recent call last):

File "D:\vnpy-2.1.7\vnpy\app\cta_strategy\backtesting.py", line 315, in run_backtesting

self.callback(data)

File "D:\vnpy-2.1.7\vnpy\app\cta_strategy\strategies\atr_rsi_strategy.py", line 129, in on_bar

df01=load_select_bar_data_from_mongodb(self.symbol,self.exchange,self.interval,(bar.datetime-timedelta(days=3)),

AttributeError: 'AtrRsiStrategy' object has no attribute 'symbol'+

+

+

4++++++++++

所以想请教大佬们,如何让策略接受到上述回测引擎engine.set_parameters所设置的属性?

变通解决方法:将bardata时间偏离设置为7小时54分。即utc_86 = timezone(timedelta(hours=7,minutes=54)),这样读取出来的数据分钟就是正常的了

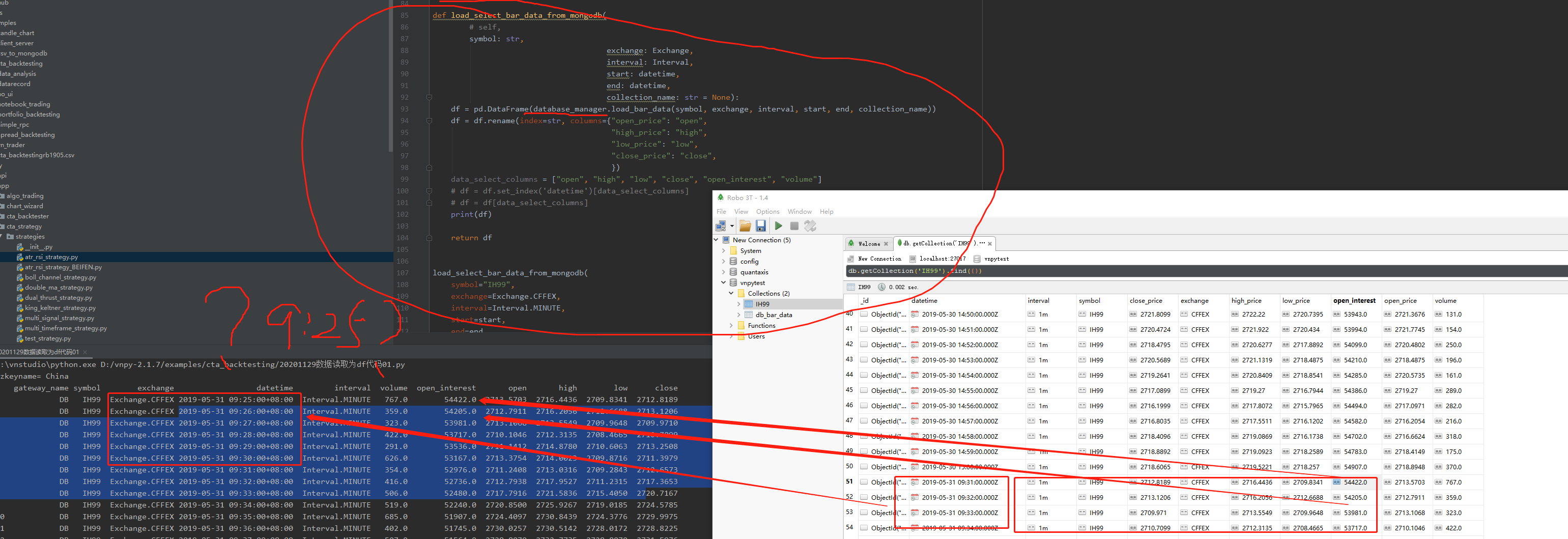

csv导入MongoDB代码如下:

from vnpy.trader.constant import (Exchange, Interval)

import pandas as pd

from vnpy.trader.database import database_manager

from vnpy.trader.object import (BarData,TickData)

from datetime import datetime, timedelta, timezone

# 中国时区是+8,对应参数hours=8

# utc_8 = timezone(timedelta(hours=8))

utc_86 = timezone(timedelta(hours=7,minutes=54))#变通

# datetime=row.datetime.replace(tzinfo=utc_8)

import pytz

tz = pytz.timezone('Asia/Shanghai')

print('tz=',tz)

# 封装函数

def move_df_to_mongodb(imported_data:pd.DataFrame,collection_name:str):

bars = []

start = None

count = 0

for row in imported_data.itertuples():

bar = BarData(

symbol=row.symbol,

exchange=row.exchange,

# datetime=tz.localize(row.datetime),

datetime=row.datetime.replace(tzinfo=utc_86),

interval=row.interval,

volume=row.volume,

open_price=row.open,

high_price=row.high,

low_price=row.low,

close_price=row.close,

open_interest=row.open_interest,

gateway_name="DB",

)

bars.append(bar)

# do some statistics

count += 1

if not start:

start = bar.datetime

print ('start=',start)

end = bar.datetime

# insert into database

database_manager.save_bar_data(bars,collection_name)

print(f'Insert Bar: {count} from {start} - {end}')

if __name__ == "__main__":

# 读取需要入库的csv文件,该文件是用gbk编码

imported_data = pd.read_csv('IH99_20101127_20201127_2.csv',encoding='gbk')

# 将csv文件中 `市场代码`的 SC 替换成 Exchange.SHFE SHFE

imported_data['exchange'] = Exchange.CFFEX

# 增加一列数据 `inteval`,且该列数据的所有值都是 Interval.MINUTE

imported_data['interval'] = Interval.MINUTE

# 明确需要是float数据类型的列

float_columns = ['open','high','low','close','volume','open_interest']

for col in float_columns:

imported_data[col] = imported_data[col].astype('float')

# 明确时间戳的格式

# %Y/%m/%d %H:%M:%S 代表着你的csv数据中的时间戳必须是 2020/05/01 08:32:30 格式

datetime_format = '%Y%m%d %H:%M:%S'

imported_data['datetime'] = pd.to_datetime(imported_data['datetime'],format=datetime_format)

品种代码='IH9902'

imported_data['symbol'] = 品种代码

# 因为没有用到 成交额 这一列的数据,所以该列列名不变

# imported_data.columns = ['exchange','symbol','datetime','open','high','low','close','volume','成交额','open_interest','interval']

# imported_data = imported_data.rename(index=str,

# columns={"时间": "datetime",

# "KQ.i@CFFEX.T.high": "high",

# "KQ.i@CFFEX.T.low": "low",

# "KQ.i@CFFEX.T.close": "close",

# "KQ.i@CFFEX.T.volume": "volume",

# "KQ.i@CFFEX.T.close_oi": "open_interest",

# })

# 筛选展示的列名

# imported_data = imported_data[["datetime","open", "high", "low", "close", "open_interest", "volume"]]

print('//',imported_data.head(1).append(imported_data.tail(1)),"//")

move_df_to_mongodb(imported_data,品种代码)+

+

+

+

不知道图能否看清

就是我数据库里没有IH99 9:25的数据,但是通过datamanager方法读取来的数据时间戳有9:25,应该是9:31才对

大佬们

我看cta的例子里面是在def on_init(self):里面self.load_bar(10) ,即获取十天的bar数据

我现想在def on_bar(self, bar: BarData):函数中,向前取2个月的数据(1分钟bardata),这时候我应该用哪个函数api来获取呢?

并同时将这两个月的1分钟bardata转为dataframe形式使用,请教一下各位大佬!

BarGenerator模块是以tick数据驱动,如果一个合约长时间没有tick数据过来将导致分钟数据缺失,应该如何解决这个问题呢,要求是实时性(分钟级别),不是盘后解决哈。

请教各位大佬如何修改BarGenerator或者通过其他途径解决呢!

def run(self):

""""""

while self.active:

try:

task = self.queue.get(timeout=1)

task_type, data = task

代码来源:vnpy/app/data_recorder/engine.py

我想请教下大佬这里关于的多线程的问题

1、在get一个task后,完成一个task后面的代码,才会取出queue中的下一个task

2、无论当前取走的task是否完成,都会在timeout=1后继续取task出来进行处理

想问下我哪个理解是正确的?或者有其他指点请赐教,感谢大佬!

def register_event(self):

""""""

self.event_engine.register(EVENT_TICK, self.process_tick_event)

self.event_engine.register(EVENT_CONTRACT, self.process_contract_event)

self.event_engine.register(EVENT_SPREAD_DATA, self.process_spread_event)

代码来源vnpy/app/data_recorder/engine.py

请教下EVENT_SPREAD_DATA这是什么数据引发的什么事件?

vnpy的1分钟行情记录是把当前tick的时间当做K线的起始时间的, 比如我要记录期货合约9:00到11:30的行情, 实际写入到数据库的行情的时间是9:00, 9:01, 9:02......11:29, 米筐数据是9.01,9.02,9.03,...11:30

请问如何修改BarGenerator源码能使其生成bar数据的时间戳同米筐数据保持一致呢,感谢!

下面是BarGenerator源码:

class BarGenerator:

"""

For:

1. generating 1 minute bar data from tick data

2. generateing x minute bar/x hour bar data from 1 minute data

Notice:

1. for x minute bar, x must be able to divide 60: 2, 3, 5, 6, 10, 15, 20, 30

2. for x hour bar, x can be any number

"""

def __init__(

self,

on_bar: Callable,

window: int = 0,

on_window_bar: Callable = None,

interval: Interval = Interval.MINUTE

):

"""Constructor"""

self.bar: BarData = None

self.on_bar: Callable = on_bar

self.interval: Interval = interval

self.interval_count: int = 0

self.window: int = window

self.window_bar: BarData = None

self.on_window_bar: Callable = on_window_bar

self.last_tick: TickData = None

self.last_bar: BarData = None

def update_tick(self, tick: TickData) -> None:

"""

Update new tick data into generator.

"""

new_minute = False

# Filter tick data with 0 last price

if not tick.last_price:

return

# Filter tick data with less intraday trading volume (i.e. older timestamp)

if self.last_tick and tick.volume and tick.volume < self.last_tick.volume:

return

if not self.bar:

new_minute = True

elif(self.bar.datetime.minute != tick.datetime.minute) or (self.bar.datetime.hour != tick.datetime.hour):

self.bar.datetime = self.bar.datetime.replace(

second=0, microsecond=0

)

self.on_bar(self.bar)

new_minute = True

if new_minute:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

else:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

if self.last_tick:

volume_change = tick.volume - self.last_tick.volume

self.bar.volume += max(volume_change, 0)

self.last_tick = tick

def update_bar(self, bar: BarData) -> None:

"""

Update 1 minute bar into generator

"""

# If not inited, creaate window bar object

if not self.window_bar:

# Generate timestamp for bar data

if self.interval == Interval.MINUTE:

dt = bar.datetime.replace(second=0, microsecond=0)

else:

dt = bar.datetime.replace(minute=0, second=0, microsecond=0)

self.window_bar = BarData(

symbol=bar.symbol,

exchange=bar.exchange,

datetime=dt,

gateway_name=bar.gateway_name,

open_price=bar.open_price,

high_price=bar.high_price,

low_price=bar.low_price

)

# Otherwise, update high/low price into window bar

else:

self.window_bar.high_price = max(

self.window_bar.high_price, bar.high_price)

self.window_bar.low_price = min(

self.window_bar.low_price, bar.low_price)

# Update close price/volume into window bar

self.window_bar.close_price = bar.close_price

self.window_bar.volume += int(bar.volume)

self.window_bar.open_interest = bar.open_interest

# Check if window bar completed

finished = False

if self.interval == Interval.MINUTE:

# x-minute bar

if not (bar.datetime.minute + 1) % self.window:

finished = True

elif self.interval == Interval.HOUR:

if self.last_bar and bar.datetime.hour != self.last_bar.datetime.hour:

# 1-hour bar

if self.window == 1:

finished = True

# x-hour bar

else:

self.interval_count += 1

if not self.interval_count % self.window:

finished = True

self.interval_count = 0

if finished:

self.on_window_bar(self.window_bar)

self.window_bar = None

# Cache last bar object

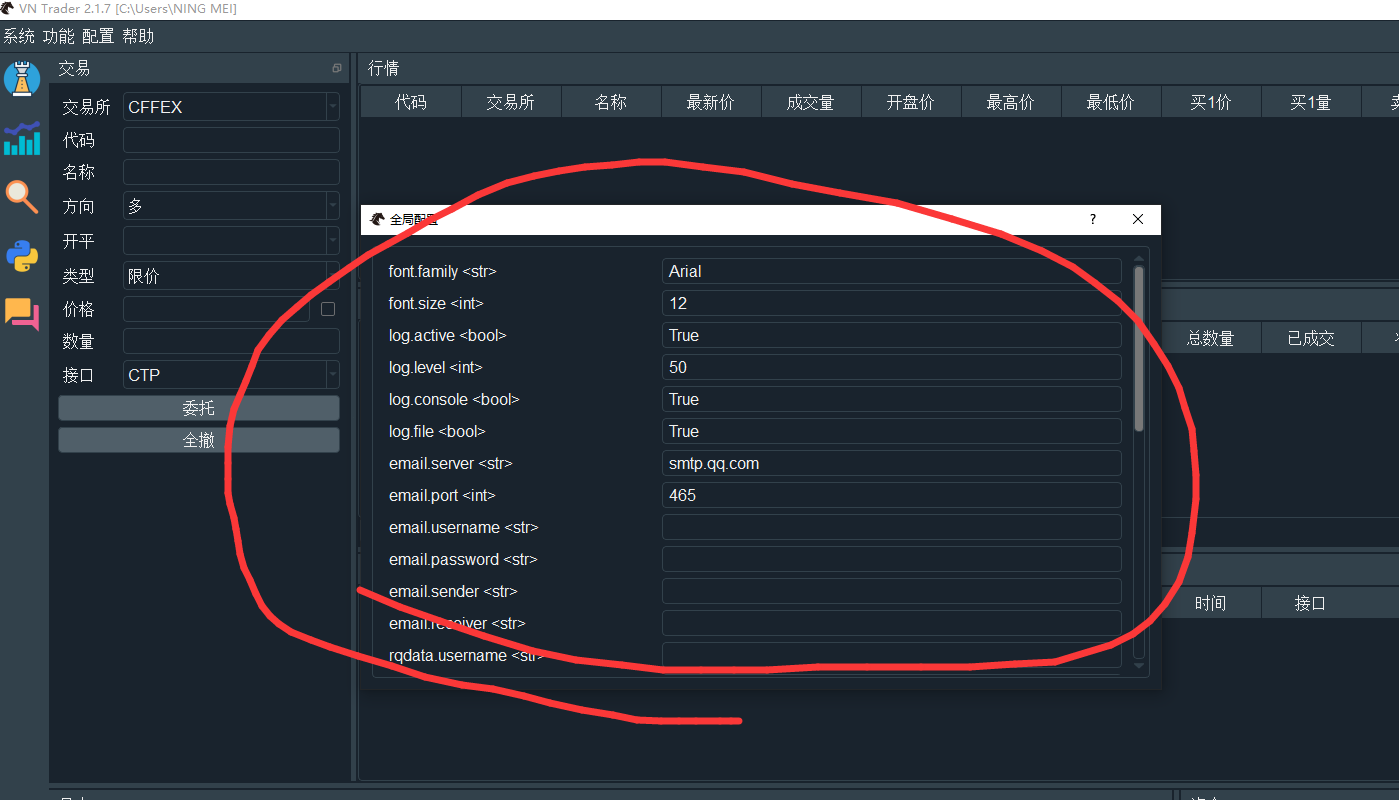

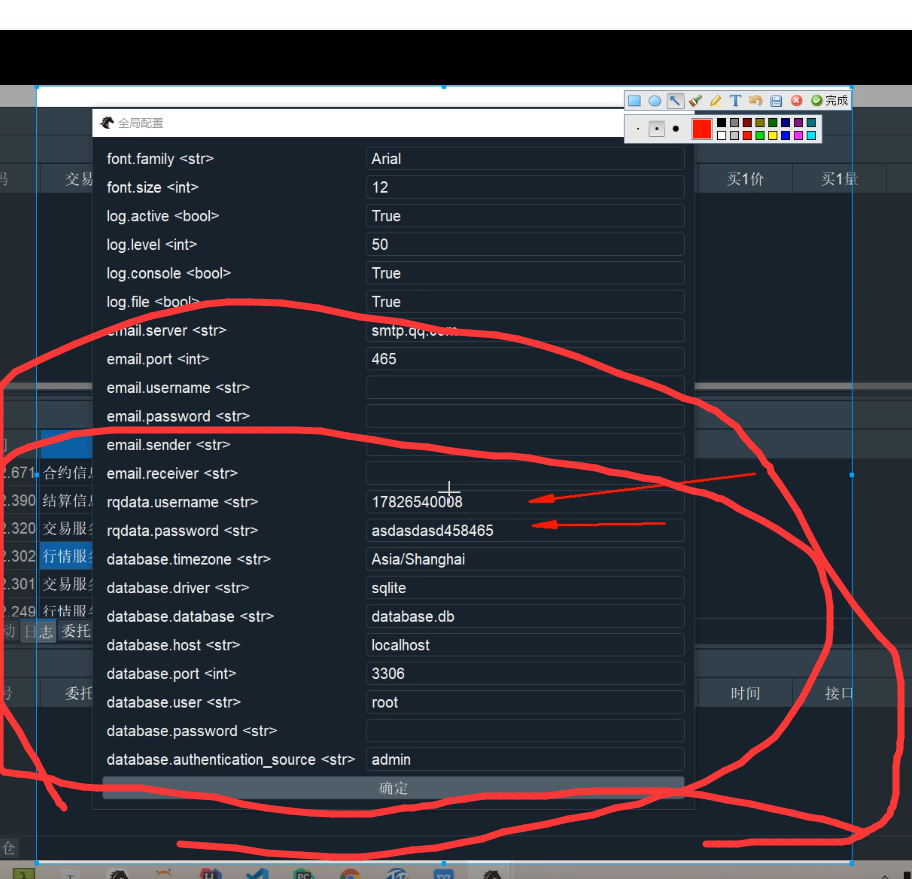

self.last_bar = bar如题我看其他视频博主 vnpy中全局配置 有数据库相关的配置,目前我在使用中的全局配置和视频博主里的不一样

我的:

视频博主的:

大佬们,我看vnpy项目库里没有单独开进程进行行情记录的demo code(论坛里好像有小伙伴说有。。),有没有大佬分享下,感谢!!

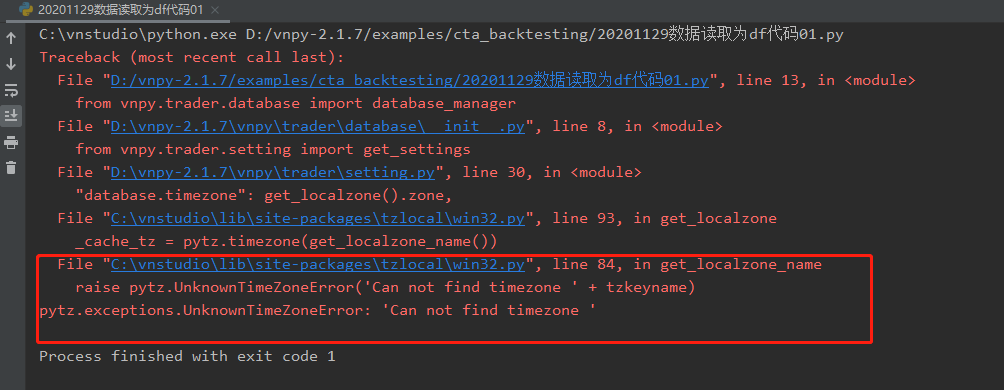

电脑win10 64位,之前的经验贴已阅读,但是这个错误前面的人没遇到

运行python -m vnstation

返回:

(VN Studio) C:\vnstudio>python -m vnstation

Traceback (most recent call last):

File "C:\vnstudio\lib\runpy.py", line 193, in _run_module_as_main

"main", mod_spec)

File "C:\vnstudio\lib\runpy.py", line 85, in _run_code

exec(code, run_globals)

File "C:\vnstudio\lib\site-packages\vnstation__main.py", line 4, in <module>

cli()

File "C:\vnstudio\lib\site-packages\click\core.py", line 829, in call

return self.main(args, kwargs)

File "C:\vnstudio\lib\site-packages\click\core.py", line 782, in main

rv = self.invoke(ctx)

File "C:\vnstudio\lib\site-packages\click\core.py", line 1236, in invoke

return Command.invoke(self, ctx)

File "C:\vnstudio\lib\site-packages\click\core.py", line 1066, in invoke

return ctx.invoke(self.callback, ctx.params)

File "C:\vnstudio\lib\site-packages\click\core.py", line 610, in invoke

return callback(args, kwargs)

File "C:\vnstudio\lib\site-packages\click\decorators.py", line 21, in new_func

return f(get_current_context(), *args, kwargs)

File "C:\vnstudio\lib\site-packages\vnstation\cli.py", line 15, in cli

run()

File "C:\vnstudio\lib\site-packages\click\core.py", line 829, in call

return self.main(args, kwargs)

File "C:\vnstudio\lib\site-packages\click\core.py", line 782, in main

rv = self.invoke(ctx)

File "C:\vnstudio\lib\site-packages\click\core.py", line 1066, in invoke

return ctx.invoke(self.callback, ctx.params)

File "C:\vnstudio\lib\site-packages\click\core.py", line 610, in invoke

return callback(args, **kwargs)

File "C:\vnstudio\lib\site-packages\vnstation\cli.py", line 20, in run

import vnstation.run

File "C:\vnstudio\lib\site-packages\vnstation\run.py", line 4, in <module>

from vnpy.trader.ui import QtGui, create_qapp

File "C:\vnstudio\lib\site-packages\vnpy\trader\ui\init__.py", line 11, in <module>

from .mainwindow import MainWindow

File "C:\vnstudio\lib\site-packages\vnpy\trader\ui\mainwindow.py", line 14, in <module>

from .widget import (

File "C:\vnstudio\lib\site-packages\vnpy\trader\ui\widget.py", line 19, in <module>

from ..engine import MainEngine

File "C:\vnstudio\lib\site-packages\vnpy\trader\engine.py", line 42, in <module>

from .setting import SETTINGS

File "C:\vnstudio\lib\site-packages\vnpy\trader\setting.py", line 30, in <module>

"database.timezone": get_localzone().zone,

File "C:\vnstudio\lib\site-packages\tzlocal\win32.py", line 93, in get_localzone

_cache_tz = pytz.timezone(get_localzone_name())

File "C:\vnstudio\lib\site-packages\tzlocal\win32.py", line 84, in get_localzone_name

raise pytz.UnknownTimeZoneError('Can not find timezone ' + tzkeyname)

pytz.exceptions.UnknownTimeZoneError: 'Can not find timezone '