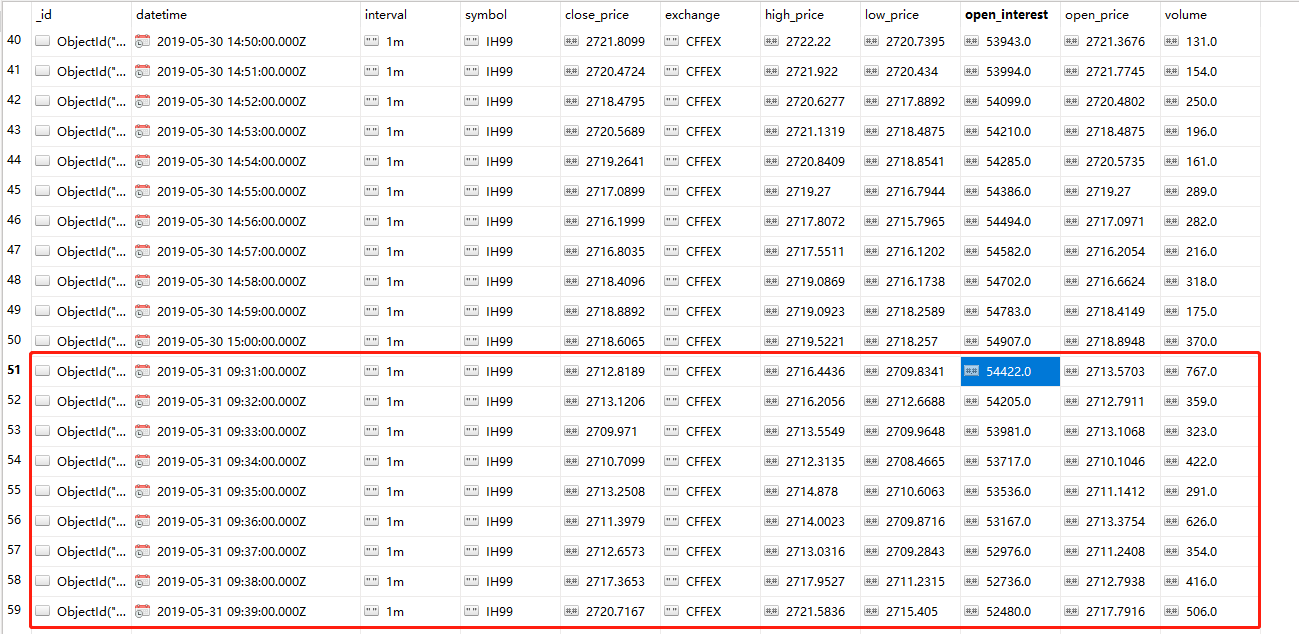

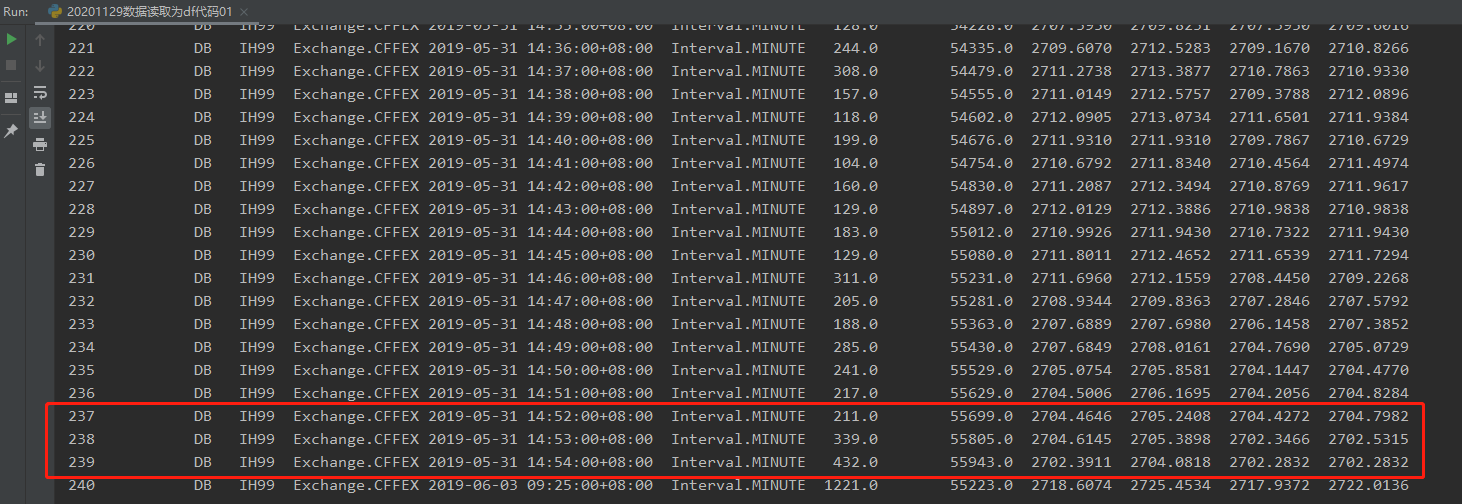

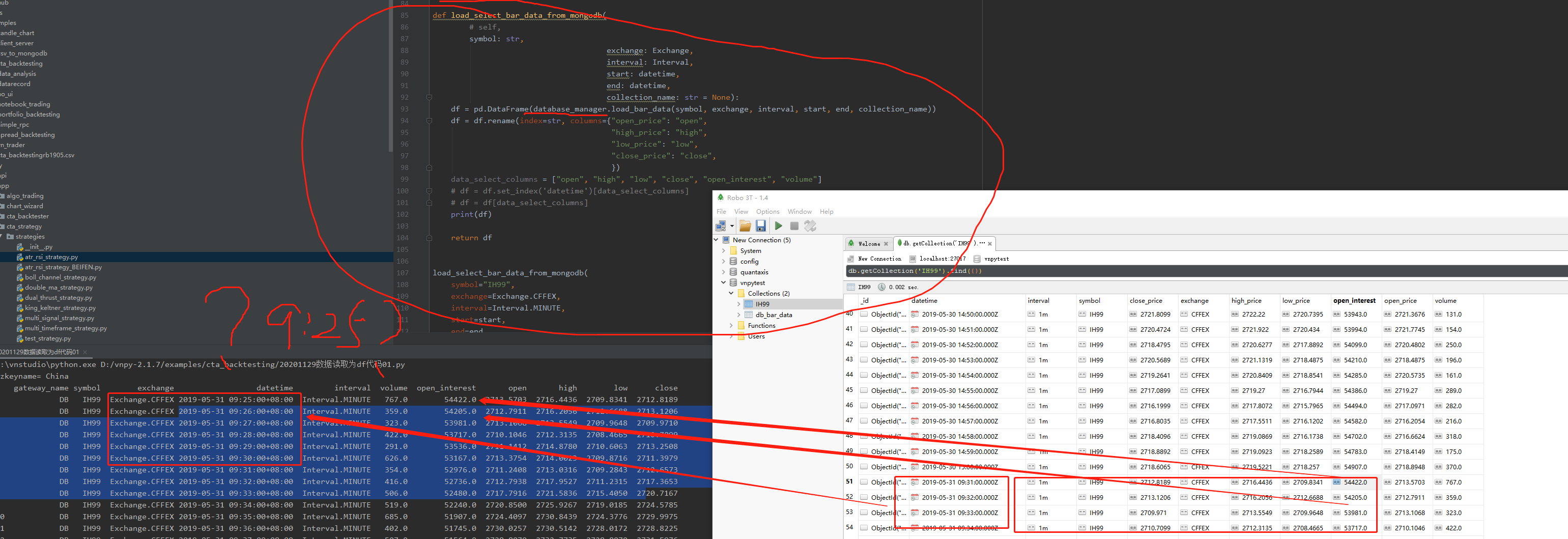

相当于整体往前移动了6分钟,很费解,读取出来的每天都是往前移6分钟

gateway_name symbol exchange datetime interval volume open_interest open high low close

0 DB IH99 Exchange.CFFEX 2019-05-31 09:25:00+08:00 Interval.MINUTE 767.0 54422.0 2713.5703 2716.4436 2709.8341 2712.8189

1 DB IH99 Exchange.CFFEX 2019-05-31 09:26:00+08:00 Interval.MINUTE 359.0 54205.0 2712.7911 2716.2056 2712.6688 2713.1206

2 DB IH99 Exchange.CFFEX 2019-05-31 09:27:00+08:00 Interval.MINUTE 323.0 53981.0 2713.1068 2713.5549 2709.9648 2709.9710

3 DB IH99 Exchange.CFFEX 2019-05-31 09:28:00+08:00 Interval.MINUTE 422.0 53717.0 2710.1046 2712.3135 2708.4665 2710.7099

4 DB IH99 Exchange.CFFEX 2019-05-31 09:29:00+08:00 Interval.MINUTE 291.0 53536.0 2711.1412 2714.8780 2710.6063 2713.2508

5 DB IH99 Exchange.CFFEX 2019-05-31 09:30:00+08:00 Interval.MINUTE 626.0 53167.0 2713.3754 2714.0023 2709.8716 2711.3979

6 DB IH99 Exchange.CFFEX 2019-05-31 09:31:00+08:00 Interval.MINUTE 354.0 52976.0 2711.2408 2713.0316 2709.2843 2712.6573

7 DB IH99 Exchange.CFFEX 2019-05-31 09:32:00+08:00 Interval.MINUTE 416.0 52736.0 2712.7938 2717.9527 2711.2315 2717.3653

8 DB IH99 Exchange.CFFEX 2019-05-31 09:33:00+08:00 Interval.MINUTE 506.0 52480.0 2717.7916 2721.5836 2715.4050 2720.7167

9 DB IH99 Exchange.CFFEX 2019-05-31 09:34:00+08:00 Interval.MINUTE 519.0 52240.0 2720.8500 2725.9267 2719.0185 2724.5785

不知道图能否看清

就是我数据库里没有IH99 9:25的数据,但是通过datamanager方法读取来的数据时间戳有9:25,应该是9:31才对

2020-11-29 23:26:59.647871 开始加载历史数据

2020-11-29 23:27:00.047876 加载进度:########## [100%]

2020-11-29 23:27:00.047876 历史数据加载完成,数据量:4560

2020-11-29 23:27:00.047876 触发异常,回测终止

2020-11-29 23:27:00.051934 Traceback (most recent call last):

File "D:\vnpy-2.1.7\vnpy\app\cta_strategy\backtesting.py", line 344, in run_backtesting

self.callback(data)

File "D:\vnpy-2.1.7\vnpy\app\cta_strategy\strategies\atr_rsi_strategy.py", line 126, in on_bar

self.load_select_bar_data_from_mongodb(self.vt_symbol,self.exchange,self.interval,(bar.datetime-timedelta(days=3)),bar.datetime,self.collection_name)

AttributeError: 'AtrRsiStrategy' object has no attribute 'exchange'

这个代码写的还不够严禁 部分属性有问题

最近问题比较多,主要就是怕自己实现的方法走弯路,低效,

所以才想跟大佬们请教一下是否是简洁有效的写法,不浪费性能,感谢

关于在策略里读取历史数据并生成dataframe的方法我写了一个初稿,请各位大佬斧正

def load_select_bar_data_from_mongodb(self,symbol: str,

exchange: Exchange,

interval: Interval,

start: datetime,

end: datetime,

collection_name: str = None):

df = pd.DataFrame(database_manager.load_bar_data(symbol, exchange, interval, start, end, collection_name))

df = df.rename(index=str, columns={"open_price": "open",

"high_price": "high",

"low_price": "low",

"close_price": "close",

})

data_select_columns = ["open", "high", "low", "close", "open_interest", "volume"]

df = df.set_index('datetime')[data_select_columns]

print(df)

return df我是准备在on_bar触发的时候调用这个函数取得想要的起止日期的dataframe

有如下两方面具体问题请请教大佬

1这个函数方法是否有必要写到比如vnpy-2.1.7\vnpy\app\cta_strategy\strategies\atr_rsi_strategy.py策略文件中 ,并设置为一个策略类的属性方法?还是说我放在类外面独立为一个单独的函数就够了?

2回测中反复从MongoDB中读取数据生成dataframe是否是一种低效的方式?有办法改进么,在同实盘保持接轨的思路下(策略是1分钟级别)?

大佬们

我看cta的例子里面是在def on_init(self):里面self.load_bar(10) ,即获取十天的bar数据

我现想在def on_bar(self, bar: BarData):函数中,向前取2个月的数据(1分钟bardata),这时候我应该用哪个函数api来获取呢?

并同时将这两个月的1分钟bardata转为dataframe形式使用,请教一下各位大佬!

用Python的交易员 wrote:

BarGenerator本身是tick驱动的,如果没有tick就合成不了了。如果硬要加上定时检查,需要额外增加定时检查的逻辑(监听EVENT_TIMER)事件,然后每秒检查当前时间和缓存K线时间戳的偏离度,超过一个水平就全部合成K线。

好的好的 谢谢大佬指导!

CTA回测引擎改造部分,我看楼主只改造了backtesting.py文件,该目录里面的engine.py里面也有loadbar,如下

def load_bar(

self,

vt_symbol: str,

days: int,

interval: Interval,

callback: Callable[[BarData], None],

use_database: bool

):

""""""

symbol, exchange = extract_vt_symbol(vt_symbol)

end = datetime.now(get_localzone())

start = end - timedelta(days)

bars = []

# Pass gateway and RQData if use_database set to True

if not use_database:

# Query bars from gateway if available

contract = self.main_engine.get_contract(vt_symbol)

if contract and contract.history_data:

req = HistoryRequest(

symbol=symbol,

exchange=exchange,

interval=interval,

start=start,

end=end

)

bars = self.main_engine.query_history(req, contract.gateway_name)

# Try to query bars from RQData, if not found, load from database.

else:

bars = self.query_bar_from_rq(symbol, exchange, interval, start, end)

if not bars:

bars = database_manager.load_bar_data(

symbol=symbol,

exchange=exchange,

interval=interval,

start=start,

end=end,

)请教一下,这个引擎engine.py要改么?

callingpulse wrote:

2020/09/09更新

原来代码bar = BarData( symbol=row.symbol, exchange=row.exchange, datetime=row.datetime,#报错的地方,需要增加时区信息 interval=row.interval, volume=row.volume, open_price=row.open, high_price=row.high, low_price=row.low, close_price=row.close, open_interest=row.open_interest, gateway_name="DB", )运行会报错:

AttributeError: 'str' object has no attribute 'astimezone'原因是新版本vnpy支持了时区数据,所以

datetime=row.datetime需要加上时区信息from datetime import datetime, timedelta, timezone # 中国时区是+8,对应参数hours=8 # 日本时区是+9,hours=9 utc_8 = timezone(timedelta(hours=8)) datetime=row.datetime.replace(tzinfo=utc_8)

一个小技巧,把bar里面的数据打印出来,看看都是什么格式。

sql_manager.get_oldest_bar_data()

大佬牛!!!出错后发现真是这个问题导致的,必须加时区

BarGenerator模块是以tick数据驱动,如果一个合约长时间没有tick数据过来将导致分钟数据缺失,应该如何解决这个问题呢,要求是实时性(分钟级别),不是盘后解决哈。

请教各位大佬如何修改BarGenerator或者通过其他途径解决呢!

梗 wrote:

log内的时间没解释清楚,以第一根bar为例:

2020-11-25 19:46:00: API_STABILITY_MONITOR: 379.240000, actual time 20:59:02.225194, num_bar = 556

19:46:00 --- 这个时bar内的datatime; 20:59:02.225194 这个是当前时间

从时间看这一根bar可以看作是非交易时间推送的fake_data,这个需要策略自己做过滤么?而2020-11-25 20:59:00 和2020-11-25 20:59:00这两根bar实际获取时间分别是 21:00:02.015919和09:00:02.269108,都在交易时间之内

2020-11-25 20:59:00: API_STABILITY_MONITOR: 380.540000, actual time 21:00:02.015919, num_bar = 2

2020-11-25 21:00:00: API_STABILITY_MONITOR: 380.240000, actual time 21:01:00.911799, num_bar = 3

这两个是tick对么?这两个不用过滤吧 要保留

BELLCOUSIN wrote:

应该就是

在vnpy/gateway/ctp/ 增加以上文件: ctp_gateway_double.py

在vnpy/gateway/ctp/init.py 导入包from .ctp_gateway_double import CtpGatewayDouble在run.py里面:

from vnpy.gateway.ctp import CtpGateway from vnpy.gateway.ctp import CtpGatewayDoublemain_engine.add_gateway(CtpGateway) main_engine.add_gateway(CtpGatewayDouble)在ctp_setting配置文件里面. 配置下ctp_setting增加下

"次行情服务器": "***.***.***.***:****",为啥我会重复推tick...

不是用hash过滤了吗

请大佬解答下我哪里步骤错了.

我觉得有可能是self.tick_buffer的问题

def run(self):

""""""

while self.active:

try:

task = self.queue.get(timeout=1)

task_type, data = task

代码来源:vnpy/app/data_recorder/engine.py

我想请教下大佬这里关于的多线程的问题

1、在get一个task后,完成一个task后面的代码,才会取出queue中的下一个task

2、无论当前取走的task是否完成,都会在timeout=1后继续取task出来进行处理

想问下我哪个理解是正确的?或者有其他指点请赐教,感谢大佬!

def register_event(self):

""""""

self.event_engine.register(EVENT_TICK, self.process_tick_event)

self.event_engine.register(EVENT_CONTRACT, self.process_contract_event)

self.event_engine.register(EVENT_SPREAD_DATA, self.process_spread_event)

代码来源vnpy/app/data_recorder/engine.py

请教下EVENT_SPREAD_DATA这是什么数据引发的什么事件?

vnpy的1分钟行情记录是把当前tick的时间当做K线的起始时间的, 比如我要记录期货合约9:00到11:30的行情, 实际写入到数据库的行情的时间是9:00, 9:01, 9:02......11:29, 米筐数据是9.01,9.02,9.03,...11:30

请问如何修改BarGenerator源码能使其生成bar数据的时间戳同米筐数据保持一致呢,感谢!

下面是BarGenerator源码:

class BarGenerator:

"""

For:

1. generating 1 minute bar data from tick data

2. generateing x minute bar/x hour bar data from 1 minute data

Notice:

1. for x minute bar, x must be able to divide 60: 2, 3, 5, 6, 10, 15, 20, 30

2. for x hour bar, x can be any number

"""

def __init__(

self,

on_bar: Callable,

window: int = 0,

on_window_bar: Callable = None,

interval: Interval = Interval.MINUTE

):

"""Constructor"""

self.bar: BarData = None

self.on_bar: Callable = on_bar

self.interval: Interval = interval

self.interval_count: int = 0

self.window: int = window

self.window_bar: BarData = None

self.on_window_bar: Callable = on_window_bar

self.last_tick: TickData = None

self.last_bar: BarData = None

def update_tick(self, tick: TickData) -> None:

"""

Update new tick data into generator.

"""

new_minute = False

# Filter tick data with 0 last price

if not tick.last_price:

return

# Filter tick data with less intraday trading volume (i.e. older timestamp)

if self.last_tick and tick.volume and tick.volume < self.last_tick.volume:

return

if not self.bar:

new_minute = True

elif(self.bar.datetime.minute != tick.datetime.minute) or (self.bar.datetime.hour != tick.datetime.hour):

self.bar.datetime = self.bar.datetime.replace(

second=0, microsecond=0

)

self.on_bar(self.bar)

new_minute = True

if new_minute:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

else:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

if self.last_tick:

volume_change = tick.volume - self.last_tick.volume

self.bar.volume += max(volume_change, 0)

self.last_tick = tick

def update_bar(self, bar: BarData) -> None:

"""

Update 1 minute bar into generator

"""

# If not inited, creaate window bar object

if not self.window_bar:

# Generate timestamp for bar data

if self.interval == Interval.MINUTE:

dt = bar.datetime.replace(second=0, microsecond=0)

else:

dt = bar.datetime.replace(minute=0, second=0, microsecond=0)

self.window_bar = BarData(

symbol=bar.symbol,

exchange=bar.exchange,

datetime=dt,

gateway_name=bar.gateway_name,

open_price=bar.open_price,

high_price=bar.high_price,

low_price=bar.low_price

)

# Otherwise, update high/low price into window bar

else:

self.window_bar.high_price = max(

self.window_bar.high_price, bar.high_price)

self.window_bar.low_price = min(

self.window_bar.low_price, bar.low_price)

# Update close price/volume into window bar

self.window_bar.close_price = bar.close_price

self.window_bar.volume += int(bar.volume)

self.window_bar.open_interest = bar.open_interest

# Check if window bar completed

finished = False

if self.interval == Interval.MINUTE:

# x-minute bar

if not (bar.datetime.minute + 1) % self.window:

finished = True

elif self.interval == Interval.HOUR:

if self.last_bar and bar.datetime.hour != self.last_bar.datetime.hour:

# 1-hour bar

if self.window == 1:

finished = True

# x-hour bar

else:

self.interval_count += 1

if not self.interval_count % self.window:

finished = True

self.interval_count = 0

if finished:

self.on_window_bar(self.window_bar)

self.window_bar = None

# Cache last bar object

self.last_bar = bar守望长城2020-6-11-艾瑞巴蒂 wrote:

个人觉得应该在执行完main_engine.connect(CTP_SETTING, "CTP")之后,在主线程中添加阻塞,以等待connect方法完全执行, 如果不阻塞一下主线程的话, 有一定的概率有部分eContract事件会先"跑掉",做不到在执行完来自oms的process_contract_event之后紧接着执行来自RecorderEngine的process_contract_event方法, 这是有风险的,最保险的做法是在主线程中增加sleep, 阻塞主线程一些时间.

问题初步解决 不能加sleep 加了就运行不了 还没搞清楚原因

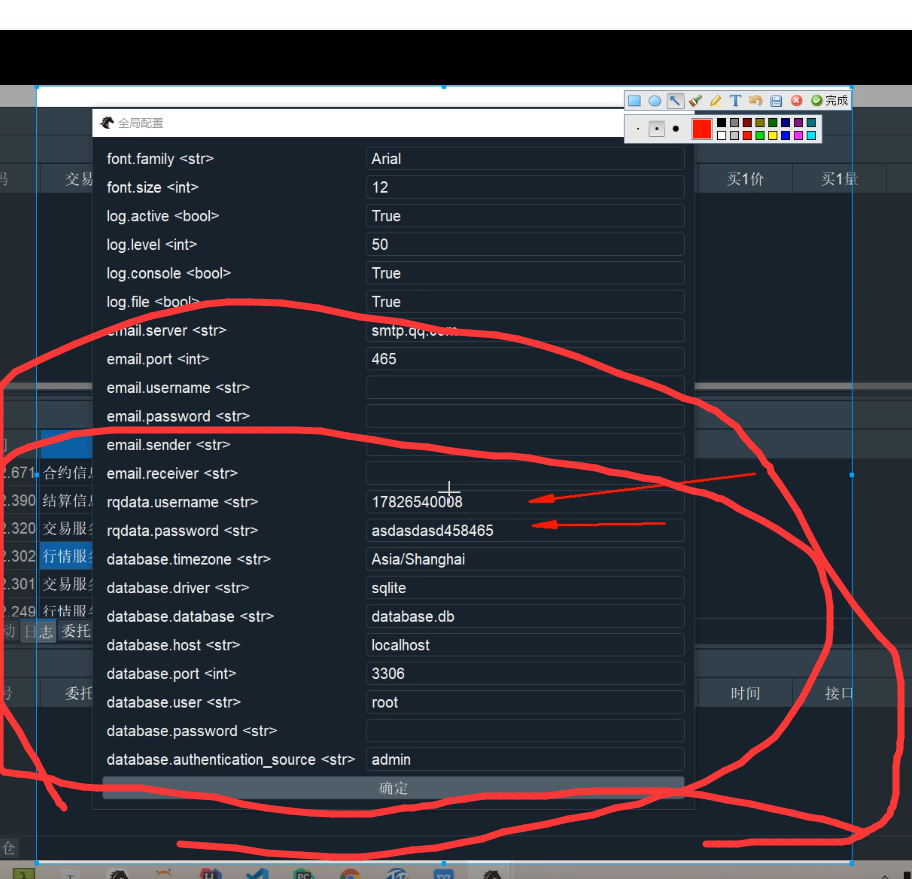

如题我看其他视频博主 vnpy中全局配置 有数据库相关的配置,目前我在使用中的全局配置和视频博主里的不一样

我的:

视频博主的:

我理解,这个行情录制代码里,新建了一个数据记录类WholeMarketRecorder,在子进程中实例了一次(但是实例的那些方法何时调用的 不清楚。。)

运行这段代码后输出如上,然后后续一直没反应,数据库中也没有数据

同时我在WholeMarketRecorder的process_contract_event方法中 写了打印合约名称,也没运行出来(说明没运行这段代码)

大佬们有空的话 方便指导下么